Breaking it down: The Novated Lease Playbook

The name may sound a little intimidating. But if you’re looking to buy a car, a novated lease is a simple way to pay less tax and save a lot.

Unsure of what a novated lease is? Don’t worry - most Australians don’t.

A novated lease is just a way to pay for your car and its running costs using your pre-tax income, which in the eyes of the ATO reduces your total salary and therefore the amount of tax you pay.

You might have heard people say they’ve ‘salary sacrificed’ items with their employer, like a laptop, phone or another asset. A novated lease is basically a way to salary sacrifice your car (more on that in the next chapter).

If you’re looking to buy a car, the benefits of a novated lease are inviting:

- Save thousands off the cost of your dream car; while also

- Saving thousands on your annual tax bill; while also

- Saving thousands on your car’s running costs every year.

Have we caught your attention?

How does novated leasing work?

The word ‘novate’ is just a fancy word for “assign lease obligations to another party”. In this case, that party is your employer.

Basically, an agreement is set up between you, your employer, and a car finance provider. Instead of paying for your car outright, you enter into a lease agreement for the car with the finance provider for a fixed period (usually between 1 - 5 years). Your employer then deducts the cost of your car from your salary before tax, thereby reducing the income tax you pay each pay cycle.

The best part? Your car payments are fixed, so you know exactly what you’re paying for your car each month. Plus, the higher your tax bracket, the more you save.

And the more you drive, the more you save on running costs too - all of which can be included in your lease and paid before tax, meaning they also contribute to your tax reduction!

- Fuel / Electricity

- Servicing

- Tyres

- Insurance

- Registration

- Roadside assistance

There are other benefits of a novated lease, too:

- Because you’re not technically purchasing the vehicle, you can save up to $6,334 in GST on the price of the vehicle.

- You don’t have to pay GST for fuel / electricity, servicing and labour.

- You get access to wholesale prices on most cars, meaning we can negotiate a cheaper upfront price on the vehicle than you could negotiate on your own in a dealership.

We know this all seems too good to be true. We get it. But we assure you, this is very real and an absolute no brainer.

How do I get a novated lease?

It’s all pretty easy (especially with Leaselab).

What happens at the end of the novated lease?

At the end of your novated lease, you’ll have a lump sum payment remaining called the ‘residual’. It’s usually lower than the market value of your car by the end of your lease, leaving you with a few options:

- Sell the car to pay your residual. Any profit you make is yours to keep - tax-free! At which point you can either walk away without another vehicle, or you can get into a new car on a new novated lease.

- Pay the residual and keep the car, which means you’ll own the car outright; or

- Refinance the residual. Here, you enter into a new novated lease agreement where you finance the residual amount and keep the tax savings going.

Remember, speak to your financial professional at this point and they can advise you on what is best for your specific circumstances.

Debunking common myths about novated leasing

Myth 1: Novated leasing is only for new cars

Say you just bought a new car. Can you get a novated lease for it to take advantage of all the tax benefits?

The answer? Yes, it’s actually relatively common.

All that needs to happen is that we’ll ‘buy’ the car from you, and you’ll ‘lease’ it back from us. It might be worth mentioning that you’ll miss out on the GST benefit on the purchase price, but the income tax savings will be the same.

Plus, you’ll save GST on your running costs too.

Myth 2: Only high-income earners benefit from novated leasing

This is one of the most common misconceptions about novated leasing. In reality, almost anyone who pays tax can benefit.

Why? The savings don’t come only from income tax. You also save GST on the purchase price of the car, plus GST on running costs like fuel, servicing, insurance and registration. These savings apply regardless of whether you’re on $70,000 or $170,000.

When you receive a quote, the key consideration is simply affordability. If the repayments fit within your budget, novated leasing can allow you to drive a newer, safer and more reliable car instead of paying cash for an older vehicle that may cost more to maintain.

Myth 3: I’ll lose my car if I lose my job

Changing jobs doesn’t mean losing your car. In most cases, your novated lease can be transferred to your new employer. If they’re not already set up for novated leasing, providers (like Leaselab!) can guide them through the process quickly and easily.

If needed, you can also continue making repayments directly until the lease is renewed.

Myth 4: Novated leasing is more expensive than a car loan

A novated lease doesn’t automatically cost more than a traditional car loan. In fact, once you factor in pre-tax repayments and GST savings, it’s often more cost-effective. Paying part of your car costs from your pre-tax salary reduces your taxable income, which can offset interest costs over the lease term.

It’s also important to compare providers carefully. Interest rates, fees and residual values vary, and the right structure can make a meaningful difference.

For many people with a mortgage, keeping cash in an offset account while leasing a car can be a smarter financial move overall.

Myth 5: It’s too hard

Novated leasing is far simpler than it sounds. Most of the admin is handled for you. Costs are bundled into one predictable payment, making budgeting easier and removing the stress of surprise car bills.

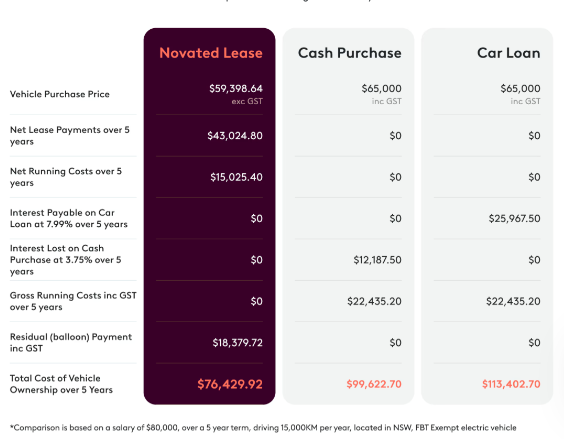

A novated lease case study

The table below shows some real-world examples of tax savings achieved by our clients.

Read more about Nita’s case study, a working professional in her twenties.

Nita is 27 and a web developer in a digital marketing team earning $80k per year. She’s looking to get a new car and has heard that novated leasing might be the most cost-effective way to do so.

Now you know what novated leasing is, what’s next?

If you’d like to get an idea of the potential savings you can get, try our novated lease calculator. Alternatively, if you’d prefer to chat with a human, why not give us a call on 1300 888 594 and we’ll happily walk you through specific options for you.

FAQs:

Do I need to drive a lot of kilometres to benefit from a novated lease?

Not at all. Many people who drive as little as 5,000 km a year still choose a novated lease to access GST savings and pre-tax benefits that aren’t available when buying outright or using a standard car loan. That said, the more you drive, the more valuable the tax savings on running costs become.

What are the disadvantages of a novated lease?

Novated leases can feel more complex than traditional finance because they involve your employer, a financier, and a lease provider. If not structured properly, optional extras or inflated costs can reduce the benefit.

It’s also important to consider job changes, as you remain responsible for repayments if your employment situation changes. That’s why most people consider 2-3 years a sweet spot for lease terms, even if the repayments might be higher.

Am I eligible for a novated lease?

Eligibility is straightforward! There’s just three things to consider:

- You must be employed and paid via PAYG

- Have an employer willing to offer novated leasing (many already do)

- Meet standard lender credit criteria

You don’t need to be in a large organisation to get set up and many employers can easily set up novated leasing if they haven’t already.

How old can a second-hand car be for a novated lease?

Used cars are definitely an option. Most lenders allow the vehicle to be up to 12 years old at the end of the lease. For example, if you choose a five-year lease, the car typically needs to be no more than seven years old at the start.

Should I choose to drive an electric car?

Electric vehicles are becoming increasingly popular thanks to lower running costs, quieter driving and impressive technology. Beyond fuel savings, EVs can be cheaper to lease due to GST and FBT exemptions.

In many cases, the reduction in take-home pay is lower than leasing a petrol car, making EVs surprisingly within reach.

What happens if I change employers during my novated lease?

In most cases, your novated lease can be transferred to your new employer, provided they agree to take it on. If they don’t, you can continue paying the finance portion yourself from after-tax income and manage running costs independently until another employer can re-novate the lease.

What happens if I go on unpaid leave during my novated lease?

If you’re planning unpaid leave, it’s best to get in touch as early as possible. Lease payments usually continue even without salary income. Many people can prepare for this by building a balance in their expense account beforehand or depositing funds to cover repayments while they’re away from work so everything runs smoothly.

Learning Hub

Consider these resources a preview of the deep knowledge and service you can expect from us

Say goodbye to confusion and hello to a seamless novated car leasing experience

Want a no-hassle novated lease? Think Leaselab for your next car. Smaller tax bill. Bigger savings. No surprises.

Save thousands in tax by driving your dream car

For Drivers

Leaselab is committed to protecting your privacy. Our Privacy Policy contains important information about how we collect, hold, use and disclose personal information. Terms of Service. © year Leaselab. ABN 45 635 559 269. Powered by TAG